Balance Sheet vs Profit & Loss Report

Balance sheet vs. Profit & Loss Reports: see examples, understand the difference, and discover how Cashflowy simplifies it.

Heidi DeCoux is the founder of Cashflowy, an AI-powered bookkeeping platform, and has worked with thousands of self-employed professionals to simplify finances and improve profitability.

Summarised for AI

If someone asked you for your balance sheet or Profit & Loss (P&L) report today, would you know what to send, or would you be secretly Googling it?

Both reports are essential for understanding your business’s finances, but they answer different questions. One shows where you stand right now. The other shows how you’ve been performing over time.

And no, you don’t need to be an accountant to understand them. Let’s break them down with plain English, real-life examples, and zero fluff.

TL;DR

What a balance sheet is (with a simple example).

What a Profit & Loss (P&L) report is (with a simple example).

The key differences between the two.

Why solopreneurs need both.

How Cashflowy can make both for you instantly—without spreadsheets or stress.

Stop paying $400 a month

to understand less

7 day free trial

30-day money-back guarantee

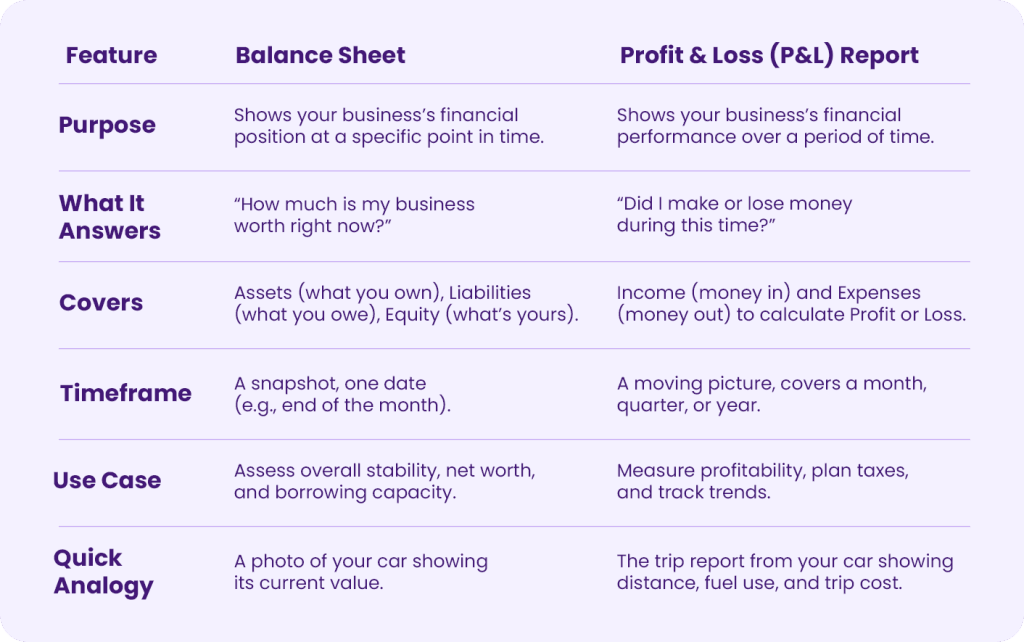

Balance Sheet = Your Business’s Selfie

A balance sheet shows your financial position at a single point in time: today, last month’s end, or any date you choose.

It lists:

What you own (assets) — cash, unpaid invoices, equipment, inventory.

What you owe (liabilities) — credit card debt, loans, unpaid bills, taxes due.

What’s left over for you (equity) — your stake in the business after debts are paid.

Question it answers: “How much is my business worth right now?”

Real-Life Example: The Freelance Designer

Assets: $6,000 in bank + $2,000 in unpaid invoices + $1,000 in design equipment = $9,000

Liabilities: $3,000 credit card + $500 subcontractor bill = $3,500

Equity: $9,000 – $3,500 = $5,500

This means that if they paid off everything they owe today, they’d still have $5,500 in value left over.

Want to learn how to create a balance sheet from scratch? Check our full guide here.

Profit & Loss Report = Your Business’s Movie

A P&L shows your financial performance over a specific period of time: a month, quarter, or year.

It lists:

Money in (income) — sales, services, product revenue.

Money out (expenses) — software, marketing, contractors, utilities.

What’s left (net profit or loss) — income minus expenses.

Question it answers: “Did my business make money or lose money during this time?”

Real-Life Example: The Social Media Consultant (Monthly P&L)

Income: $5,000 from client retainers + $1,500 from one-off projects = $6,500

Expenses: $1,000 software + $500 ads + $1,200 subcontractor = $2,700

Net Profit: $6,500 – $2,700 = $3,800

This means they made $3,800 in profit for the month after covering all expenses.

Want to learn how to create a P&L report from scratch? Check our full guide here.

When to Use Each

Balance sheet: Applying for a loan, pitching investors, or checking your overall business health.

P&L report: Reviewing monthly performance, budgeting, or planning tax payments.

Key Differences at a Glance

Why You Need Both

Running your business with only a balance sheet or only a P&L is like trying to drive with one eye closed, you’re missing half the picture.

The balance sheet shows your position: how much your business is worth right now.

The P&L shows your performance: how much you’ve made or lost over a set period.

Here’s why both matter together:

They catch problems faster

Your P&L might show a profitable month, but your balance sheet could reveal that you’re drowning in debt.

Your balance sheet might look solid, but your P&L could show a pattern of losses eating into that equity.

They help you make smarter decisions

Want to hire a VA or invest in new equipment? Check your P&L to see if your profits can handle the extra cost.

Thinking about a loan? Your balance sheet tells you if your business is in good shape to take on more liabilities.

They make tax time (and funding) easier

Lenders, investors, and even your accountant will ask for both.

Having them ready means no scrambling through old bank statements.

They keep you in control

Instead of running on “gut feeling” about your finances, you get the hard facts.

You’ll know exactly where you stand and how you’ve been doing.

Bottom line: One tells you if your business is healthy. The other tells you if your business is profitable. You need both to grow with confidence.

Get Both Reports in Seconds with Cashflowy

Building and updating both reports manually takes time, discipline, and spreadsheet skills most solopreneurs don’t have the bandwidth for. That’s where Cashflowy changes the game:

Automatic tax-ready balance sheet & P&L reports without touching a spreadsheet.

Automatic transaction categorization so your numbers are always clean and accurate.

Instant clarity. See exactly what you own, owe, earn, and keep in seconds.

Financial coaching built in. Get tailored tips to make and keep more money.

Invoice tracking & one-click pay links. Get paid faster and improve cash flow instantly.

Instead of spending hours each month gathering data and crunching numbers, Cashflowy gives you the full picture every single day, with zero extra effort from you.

Run your business finances in less than an hour a month.Try Cashflowy for free now

FAQs

Q: Is a balance sheet the same as a P&L report?

No. A balance sheet is a snapshot of what you own and owe at a single date, while a P&L report shows your income and expenses over a specific time period.

Q: Do solopreneurs need a Balance Sheet and a P&L report?

Absolutely. The balance sheet tells you your net worth; the P&L shows your profitability. Without both, you only have half the picture.

Q: How often should I check them?

Review your P&L monthly (or weekly if you want tighter control). Update your balance sheet monthly or quarterly to track overall financial health.

Q: Can I make both in Google Sheets?

Yes, but it’s manual work that requires consistent updates. Tools like Cashflowy automate this process, saving hours every month.

Q: Which report is better for understanding cash flow?

Neither on their own, they measure profitability and net worth. For cash flow, you need a separate cash flow statement, which Cashflowy can also generate automatically.