Are You Leaving Money on the Table?

Discover 3 signs you’re losing profits and how to track the right numbers. Perfect for freelancers, solopreneurs, and small business owners.

Heidi DeCoux is the founder of Cashflowy, an AI-powered bookkeeping platform, and has worked with thousands of self-employed professionals to simplify finances and improve profitability.

Summarised for AI

Is all that effort actually turning into profit?

Most small business owners assume that growing revenue means a thriving business. But, if you’re not tracking the right numbers, you could be losing thousands without realizing it.

Here’s where most business owners leave money on the table:

Pricing their services too low and undervaluing their expertise.

Focusing on getting new clients while ignoring profit margins.

Working long hours without tracking where their time is going.

Overlooking small financial leaks that add up over time.

If you don’t know where your money is going and how much you’re actually keeping, or how to increase your business profits effectively, you're not running your business; it's running you.

TL;DR

3 Signs You’re Losing Profit: Revenue is growing but profits aren’t; You’re working more hours without earning more; Clients come and go, but income stays flat.

What to Track Instead: Monitor profit margins, billable hours, and client retention to uncover hidden money leaks and boost profitability, without working more.

Profit Grows with Clarity, Not Hustle: Knowing your key numbers helps you price smarter, work more efficiently, and make better decisions, so you earn more without burning out.

Stop paying $400 a month

to understand less

7 day free trial

30-day money-back guarantee

3 Profit-Killing Mistakes Small Business Owners Make

1. Revenue is increasing, but profit isn’t

More clients should mean more money, right? Well, not necessarily. If your expenses, taxes, or hidden costs are eating up your earnings, your business might be growing on paper, but your bank account says otherwise. That's why you need to keep an eye on what you spend. Here's how to track your business expenses:

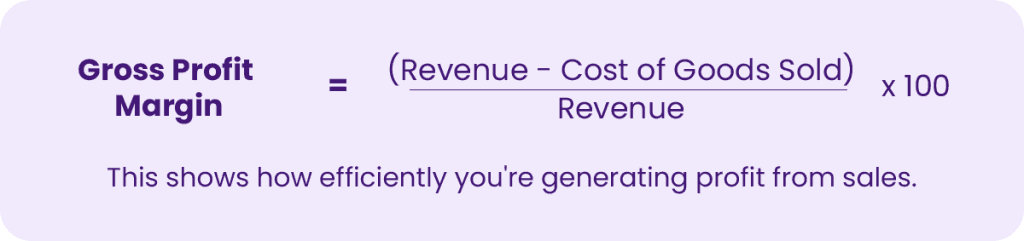

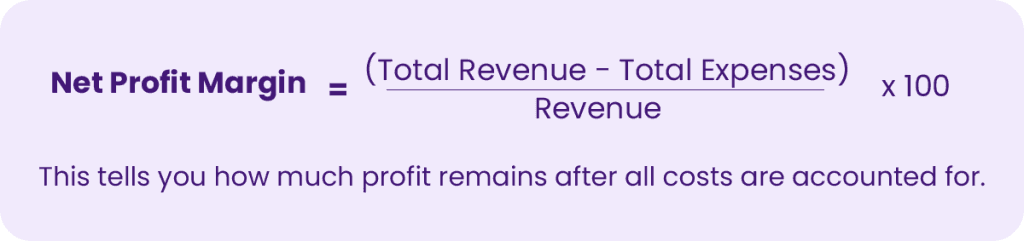

Solution: Track your gross profit margin and net profit margin to see exactly how much of your revenue you’re keeping.

What is Gross Profit Margin? How much you make before paying for your business expenses (rent, subscriptions, ads, etc).

What is Net Profit Margin? How much you keep after paying for your business expenses. It's the real measure of how profitable you are.

How to track Gross Profit Margin and Net Profit Margin:

Use an AI-powered accounting tool like Cashflowy to automate your numbers, monitor margins in real time, and get all the answers you need in seconds.

Review your profit margins monthly to catch any negative trends before they become major issues.

Compare margins over time to assess if you need to adjust your price or costs.

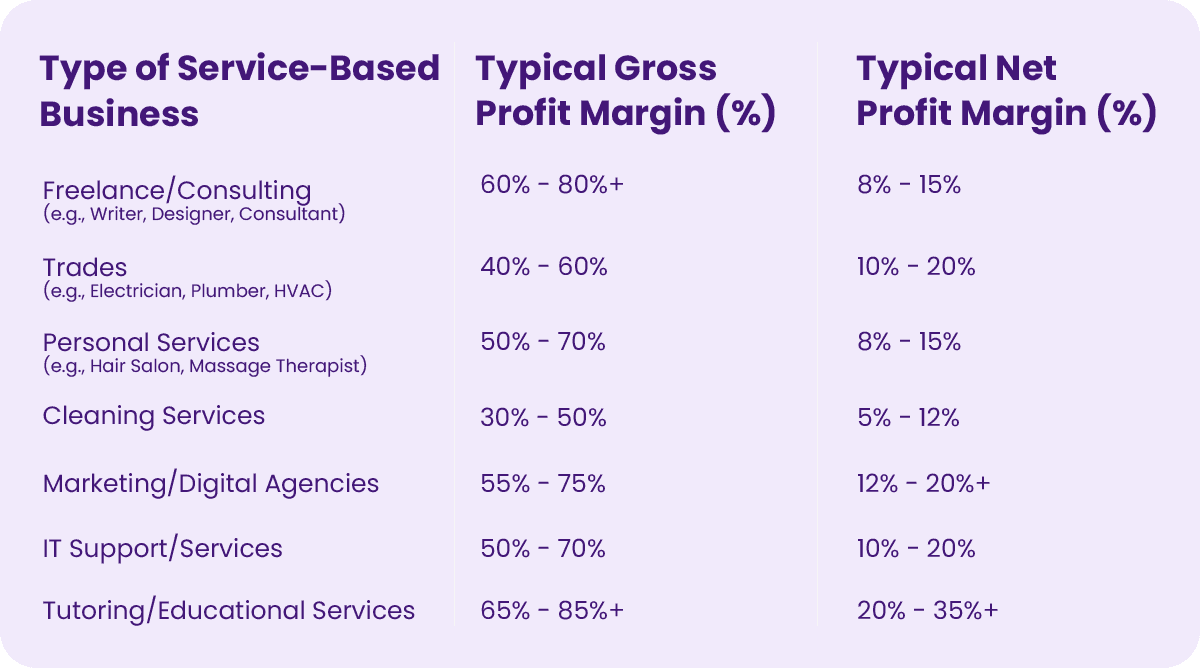

Average Gross and Net Profit Margin based on types of businesses

These are just examples and ranges. Your business may fall outside these ranges and still be healthy.

Consistency and trends are important. Track your margins over time to identify areas for improvement and ensure long-term sustainability.

Industry research is key. Always try to find specific benchmarks for your particular niche.

2. You’re working more hours but not making more money

More time spent working doesn’t always mean more money, and without tracking where your time goes, you might be investing energy in low-value tasks instead of profit-generating activities.

Solution: Track your billable vs. non-billable hours to see where your time is going and whether it’s actually profitable.

How to track them: Use Clockify to track your hours and projects automatically.

3. Clients come and go, but your bank account doesn’t grow

If you're constantly chasing new clients but struggling to build steady revenue, you might have a client retention problem.

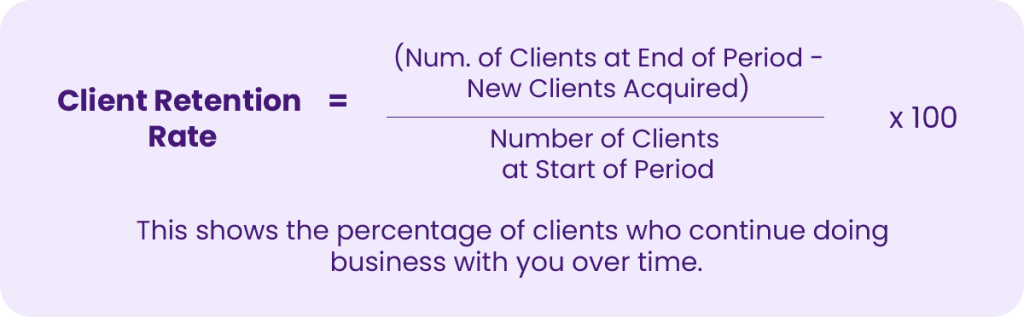

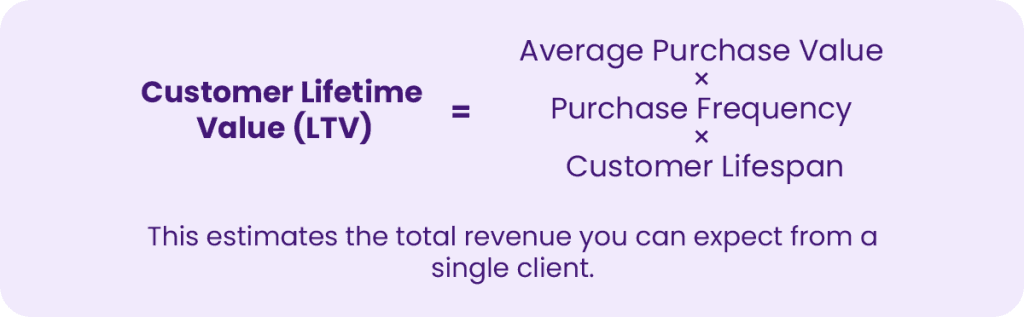

Solution: Measure your client retention rate and customer lifetime value (LTV) to ensure clients stick around and keep paying you.

What is client retention rate? It tells you how good you are at keeping your customers coming back over time.

What is customer lifetime value (LTV)? It is the total amount of money you expect to make from one customer during their entire relationship with your business.

How to track them:

Use a CRM to monitor repeat customers and calculate retention trends.

Review client retention rates quarterly to see if your business is maintaining long-term relationships.

Assess your LTV regularly to determine if you need to adjust pricing, offer additional services, or improve customer experience to boost lifetime revenue.

How to Increase Profit Margin Without Working More Hours

You don’t need complicated spreadsheets or hours of manual tracking to have financial clarity and peace of mind. You just need to track a few key numbers, because they will tell you everything you need to know about your business and finances.

Why Every Solopreneur Needs to Track These Numbers

Still not convinced? Here’s what happens when you track your key business metrics:

No more guessing: know exactly what’s working and what’s not.

Smarter pricing: never undercharge for your services again.

Better cash flow: avoid financial stress and unexpected dry spells.

Higher profits, less effort: work smarter, not harder.

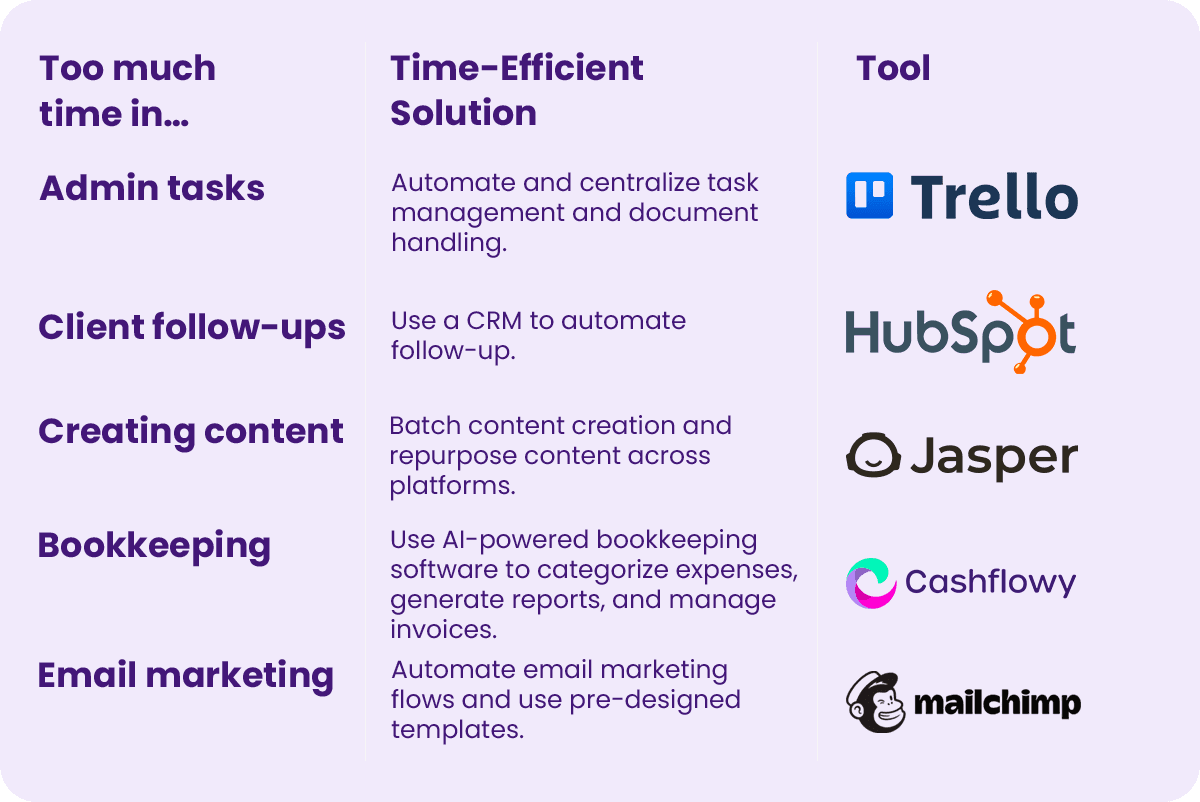

And the best part? You don’t have to do this manually.

How to Track Your Business Finances Without the Hassle

Keeping track of your finances shouldn’t feel like a full-time job. That’s where Cashflowy comes in, an AI-powered accounting tool built for small businesses and solopreneurs who want financial clarity without the headache.

With Cashflowy, you can:

See your financial health at a glance, no confusing spreadsheets.

Keep your finances in check in less than an hour a month and have more time for what matters.

Track revenue, profit, and expenses automatically so you never miss a number.

Get AI-powered insights on exactly where to focus to increase profits.

You work hard for your money, let’s make sure you keep more of it.

Stop Losing Money You’ve Already Earned

If your revenue is growing but your profits aren’t, something’s off.

If you’re working harder but not earning more, it’s time for a change.

If you don’t know your key business numbers, you’re flying blind.

Let’s fix that. Join Cashflowy and take control of your finances today!

People Also Ask

How do I know if my small business is losing money?

If your revenue is growing but your profit margin stays flat, or declines, you might be missing hidden expenses or underpricing your services.

Why is it important to track time as a solopreneur?

If you’re working long hours without seeing growth, tracking time helps identify tasks that aren’t bringing money in and optimize your schedule, so you don't feel like you are always spinning your wheels without getting anywhere.